Whether you are working in the FMCG, Technology, or Manufacturing Industry, almost every business uses GPM – gross profit margin analysis to analyse its financial performance in terms of procurement, pricing, & profitability. This mere indicator aids in understanding the underlying reasoning behind deteriorating GPM.

COGS – Cost of goods sold

COGS – Cost of goods sold refers to the direct costs incurred to produce the goods & services produced by the Company to earn profits e.g. manufacturing cost of a Smart-phone will include the following direct costs.

Stakeholders:

In any given business the key stakeholders interested in the COGS would be the likes of FP&A – financial analysis & planning dept, pricing analyst, & sales & marketing dept.

FP&A is involved in the budgeting & forecasting of the business & need key COGS information to be able to produce reliable forecasts for the senior management.

Pricing analyst are involved in the pricing of the company’s products & services.

Sales & marketing departments have to have good visibility in order to ensure that the products & services are sold at competitive rates in order to sustain stable gross margins.

GM – Gross Margins

GM % = Sales LESS Direct costs/Sales*100

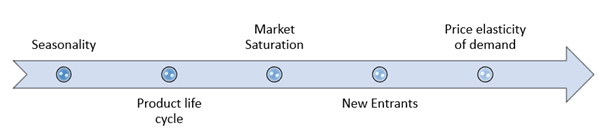

Gross margin analysis is very important KPI – key performance indicator for any given business. If gross margins are dropping it may indicate that the direct costs are increasing & leading to lower GM. It may not be feasible to increase prices to offset the decrease in GM.

It could be that the product life cycle has reached its saturation stage & margins have started to deteriorate given the change in customer choices.

It could well be true that the new competitor products & services are being offered at more competitive prices.

Seasonality plays a vital role to determine the demand for a particular product e.g. ice-cream sales in summer, warm clothing in winter.

Conclusion

COGS – Cost of goods sold & the underlying gross margins – GM analysis is therefore imperative to manage any business. Normally the folks in the FP&A – financial planning & analysis or BP&A – Business planning & analysis are involved in scrutinising these two areas of the profit & loss account.

Being a Management Accountant, you will always come across these terms & will have to consider your particular industry to reach any forgone conclusions. Though the key factors to bare in mind are seasonality, product life cycle, new entrants, substitutes of products & services you are offering, & the price elasticity of demand.