The ‘Building Blocks’ of streamlining a robust ‘BS – Balance sheet reconciliation’ system should not be undermined in this day & age. Whereby Companies are always having to adapt to new advancements (ERP/RPA) & regulatory regimes (Brexit/ IFRS). Needless to say, but the current global scenario amid Covid-19 is no exception. Hence, the importance of having an agile ‘Balance sheet reconciliation’ process cannot be over-emphasised. Perhaps you have heard about the off-balance-sheet measures of ‘Enron & WorldCom’; which led to ‘SOX – Sarbanes Oxley legislation’ in 2002. Maintaining a ‘robust’ balance sheet reconciliation system is imperative, to ensure there are no ‘bottlenecks’ during period/year end, to substantiate ‘account balances’ for the preparation of Statutory Accounts (SOCI, SOFP, SOCF).

Usually the balance sheet reconciliations are prepared after the month end e.g. in the first week following the month end. Depending on the size & magnitude of COA – chart of accounts of a particular company; the underlying process of balance sheet reconciliation can be a time-consuming exercise. Financial Accountants seldom find themselves under great pressure to produce timely BS recs along with supporting documentation to ensure the underlying FS – Finance Statements have transparency. Collating the supporting documentation/backups (bank statements, invoices, creditnotes) to support key BS recs can be a daunting experience.

Fortunately, the role of preparer & reviewer of balance sheet reconciliations has been automated by a system called ‘Blackline’. This system is being used by many Companies to automate their balance sheet reporting process & mitigate any material misstatements, before publishing their final accounts.

From Preparers perspective though, there are various underlying considerations that are to be bear in mind e.g. whether a particular reconciliation includes an account summary, whether the underlying reconciliations have been reviewed & signed off (SOX), and should a reconciliation include ‘notes’ regarding any adjustments (write offs) that are being made or any errors that are being corrected (reversal of accruals).

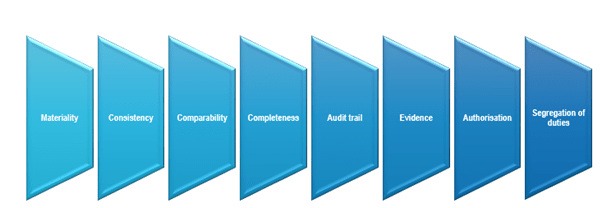

The ultimate purpose of ‘balance sheet reconciliation’ process is to provide an audit trail of all account movements, restatements, & adjustments in-line with the GAAP – generally accepted accounting principles. This can be achieved by regularly reviewing the reconciliation matrices & by ensuring that the ‘errors of omission/ commission/ principle’ have been rectified. Reviewers deploy various tests to substantiate the correctness of BS account reconciliations e.g. materiality, completeness, evidence, authorisation & consistency.

Best Practices:

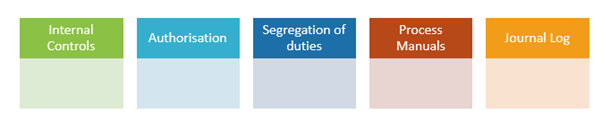

By deploying the following ‘BP – Best practice’ procedures, Accountants can enhance the control environment of a Company as far as the transparency of financial statements is concerned and help mitigate the risks of material misstatements & overriding of controls, whether due to fraud (intentional) or error (unintentional).

- ‘JL – Journal Logs’ should include a complete log of journals inputted by the finance team during a particular calendar month e.g. date, person inputted by, & description of a journal.

- ‘PM – Process Manuals’ are a statutory requirement under some reporting jurisdictions (SOX). PM assist in bridging the knowledge ‘gap’ that is created, when key personnel leave the company & leave a knowledge-gap. Process manuals are a good way of ensuring that an organisation is always on the look-out for ‘continuous process improvements. Whether that be the ‘standardisation’ or ‘automation’ of key accounting processes e.g. using VBA – macros or BI – Business intelligence’ functionality in Ms Excel to automate repetitive accounting tasks.

- ‘SOD – Segregation of duties’ is imperative as this leaves no room for overriding of controls. There should be procedures in place to ensure that tasks are shared between staff e.g. an Accounts assistant prepares the account reconciliation, an accounting Supervisor then performs a first line of review & finally a Finance Manager undertakes the 2nd tier review to ensure full compliance with the underlying accounting policies & procedures.

- Make sure there is no room for complacency & the BS recs (discrepancies) are ‘reviewed’ & scrutinised with professional scepticism to leave no room for material misstatements.

- IC – Internal controls should be developed & embedded within the policies & procedures of a Company e.g. Procurement of products & services (P2P- purchase to pay), Reimbursement of employee expenses, & management of Company Credit Cards (Concur).

In conclusion, it is imperative that Accountants develop ‘agile accounting processes & procedures’ to ensure that underlying accounts are always scrutinised & reviewed with professional scepticism. Else the ‘Balance sheet reconciliation’ process will merely be a ‘box-ticking’ exercise.