Some SME Companies take exemption from preparing a SOCF – Statement of Cashflow in their Statutory-accounts under UK-GAAP (FRS-102 reduced disclosure). Given the current economic climate amid Covid-19 it’s imperative that Companies take cash-flow forecasting seriously to enable them to ‘foresee’ their financial-commitments & avoid any potential road-blocks.

Inherently, cash-flow challenges are more-prevalent in the ‘service-industry’ given the nature of its very business-model. A small Consultancy-business may allow lenient customer-credit-terms to boost-sales & realise that customers do not pay till the last minute. Whereas the Consultancy may have acquired the external products & services from its own suppliers to deliver the ‘projects’ & only to be told that they will not be paid on time. This kind of bottleneck-situation puts Consulting businesses under severe pressure. Thus, the need to prepare a regular cash-flow-forecasts cannot be overemphasised.

There are two ways you can prepare a cashflow statement, namely ‘Direct & Indirect’ method. In practice, most of the Companies use Direct-method.

Under Direct-method: cashflows are shown as ‘Outflows – payments’ & Inflows -receipts.

This is based on the operating cycle of a business i.e. what you pay to your ‘suppliers’ to hire ‘products & services’ to run your business & what you sell to your ‘customers’ to earn-cash.

You could also think of this as your ‘working-capital’. Imagine the current economic-climate, how many businesses will be going through ‘working-capital’ problems due to volatile-sales & fixed running-costs.

Under Indirect-method: cashflows are shown, when cash is paid/received, unlike the financial statements which are prepared on ‘accrual’ basis. Therefore, under this method adjustments are made to eliminate the impact of accrual-basis by adding back Non-cash items e.g. depreciation & impairment of long-term-assets.

IAS 7 – Statement of cashflow

Following are the three building-blocks of preparing a cash-flow statement under Direct-method:-

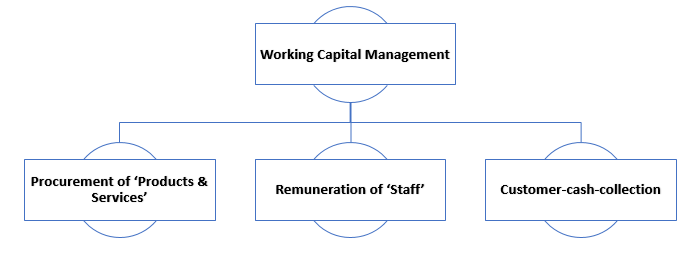

Operating Cashflows – Working Capital: As far as operating-CFs are concerned, Companies need to ensure that strict controls are in place to manage working-capital requirements e.g. to pay suppliers & employees for their products & services respectively.

When preparing the Operating-CF section, you need to ensure that you identify & count Company’s operating activities vigilantly: –

- Suppliers: When a business acquire products & service to run their business e.g. payments for rent & rates, leases, HMRC taxes, & business insurances.

- Employees: Compensation paid to employees.

- Customers: This includes the cash received from customers for providing products & services.

Outflows – payments to suppliers & employees for acquiring their products & services alike.

Inflows – payments received from customers for providing products & services.

Inherently, the likes of Small businesses are at the forefront of cashflow challenges. This could be due to free-style-opportunism work-ethic of their Owners, who may not find it necessary to use ‘quantitative-forecasting’ techniques to anticipate future cash -flows.

Another example is when Companies are just starting-off & launching their products & services with no real cash-flow planning. Customer credit terms may be too lenient leading to delays in cash collection process & ultimately damaging Company’s working-capital.

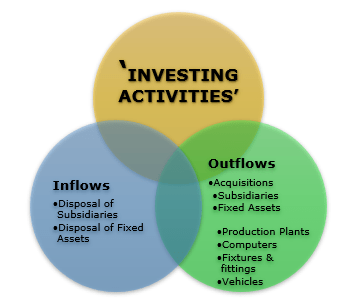

Investing Cashflows – Acquisition of Assets to enhance Business Operations

Based on the working-capital position, Companies decide whether they have the means to enhance their operating-capacity to target a new-market. This in turn lead to acquisition of Subsidiaries, Fixed-assets & other Investments e.g. an installation of new plant to increase production facility.

In the ‘investing-CF’ section your job is to ensure that you correctly present such cashflow-activities. You need to assess whether a fixed asset has been purchased or disposed during a financial year. What new initiatives have been taken e.g. purchase of plant, vehicles, computers etc.

Inflows – cash collected upon sale of fixed assets

Outflows – cash paid to acquire fixed assets

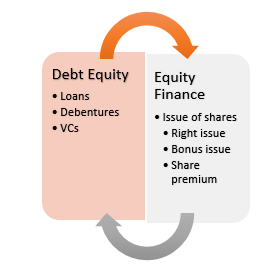

Financing Cashflows – Financial instruments to raise Capital

In the current economic climate, a majority of Small Business are encountering cashflows challenges & reverting to financial institutions for help. Therefore, the importance of having a strict control in place to manage the working-capital requirements cannot be undermined.

The usual means of acquiring finance remains to be debt-financing, or equity-financing.

Where debt-financing can be related to ‘bank-loans’ whereas equity-finance can be thought of as ‘issue of shares or capital-contributions by the Company Owners.

Inflows – cash received by means of debt/equity-loans.

Outflows – cash paid towards the repayment of debt/equity loans.

In summary, over 70% of Small businesses face cashflow hiccups as they start to scaleup drastically without being mindful of their financial obligations & commitments. Predominantly, Consultancy-Industry is renowned to encounter cashflow-challenges. This is because the bulk of their work is performed & invoiced in stages (WIP). Unlike Retail & FMCG businesses where cash is collected simultaneously at the time of sale (Amazon/eBay).