There is a perception that in order to exploit the lower tax rates of tax-havens, a large number of Large Multinational Corporations divert profits to ‘Foreign Subsidiaries’ which are based in tax-havens. The Organisation-of Economic Cooperation & development – OECD has laid out core Transfer Pricing guidelines & rules, that are to be followed by Organisations using ‘Transfer Pricing’ mechanism to transact with fellow Companies (Parent/Subsidiaries/Associates).

There has been an increasing trend in adapting an SSC- Shred-Service-Centre Business Model, whereby an SSC is created to provide Centralised-Services (R&D, Marketing, HR) to the Group. Hence the need to implement Transfer-Pricing & intercompany policies & procedures is inevitable.

Intercompany Accounting:

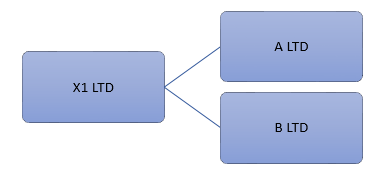

- Intercompany accounting is used, when Companies transact with each other e.g. ‘Parent’ buys goods/services from its Subsidiary or a ‘Subsidiary’ acquires goods/services from its Sister-Company.

- OECD regulates the Transfer-pricing legislation in Europe that Companies need to follow in order to be compliant with OECD-Transfer-pricing (intercompany loans) Legislation.

Intracompany Accounting:

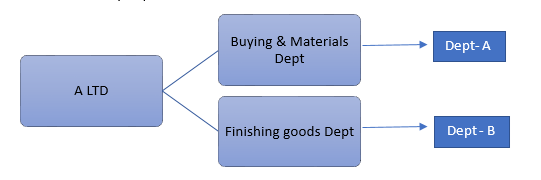

- However, if the transaction is between a Department/Group of a same legal entity then it’s called an INTRACOMPANY-transaction. Notably the mechanics around intracompany are decided by the relevant management of that Company e.g. in Company X1 , Dept-A sends goods to Dept-B for enhancement before shipping them to the end-customer. Since this transaction takes place within a same Company & the management of the Company decides as to what percentage Dept-B should charge to Dept-A for providing the services asked by Dept-A.

Intercompany AGREEMENTS:

- In Large Multinational Organisations the underlying Intercompany transactions are agreed by drawing up intercompany agreements between different legal-entities of the Group.

- An Intercompany-matrix is then drawn up to ensure the correct accounting of these intercompany transactions e.g. use of accounting codes, cost centres, & foreign exchange rates.

- Senior Management (FM/FC/FD) is involved in the setting up of these intercompany agreements to ensure that Group follows ‘arm’s length principle’ as laid out by OECD.

Intercompany Reconciliations (NETTING OFF):

- To ensure there are no abnormal intercompany balances at the month/year end; companies should put in place a robust ‘Netting-off’ process, wherein the two sides of an intercompany truncations net off to Zero.

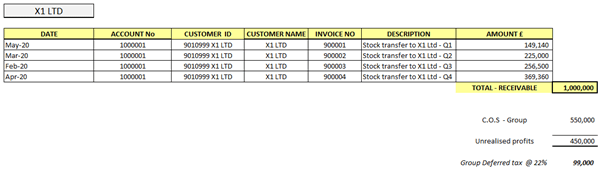

Example:

X1 LTD’ sold goods to A Ltd for £1000,860K. These goods were purchased for £550K by X1 Ltd leading to unrealised profits of £450k at Group level.

Disagreements:

- The intercompany transactions should be monitored in line with the intercompany agreements. Therefore, it’s imperative to document intercompany agreements to avoid any disagreements afterwards.

- The likes of Financial Controllers & Finance Directors are involved in the mediation process, to ensure there are no disagreement when it comes to settle intercompany balances between different legal entities of a group. These disagreements may arise due to one Entity charging higher mark-up to its Sister Company.

- In an Organisation with more divisional-structure setup, this kind of disagreements may be more prevalent as managers are appraised on their divisional-performance. Their view could be obscured by tunnel-vision. Whereby they would want to ensure their division has the higher rate of profitability. This is to guarantee that they get their performance related perks (bonus, profit share).

Best Practices:

- To ensure Intercompany-agreements are documented & reviewed regularly. Normally before the annual budgeting process to ensure that any underlying intercompany relationships are identified & accounting scope & ways of working are agreed by the Senior Management.

- End-to-end-allocation-of-tasks e.g. PO, preparer, reviewer, & mediator for intercompany disagreements.

- To ensure there is a smooth Netting-off process in place. Wherein the intercompany balances are Eliminated-upon-Consolidation (SAP- BPC, Oracle-Khalix)

- Regular review & reconciliations are performed to ensure there are no abnormal balances & accounts are free from material misstatements whether due to fraud or error.

- OECD-guidelines of arm’s length principle are always followed, when it comes to price the transactions with legal entities that are part of the same group.

In Summary, there has been rise in adapting Shared Services mechanism in many Multisite Corporations. Many International Corporations have been creating Shared Service Centres – SSC in Eastern Europe & South East Asia. This has led to the use of Transfer pricing methodology to price intercompany transactions & SSC recharges. Though there is great room for improvement as far as compliance with OECD guidelines is concerned.