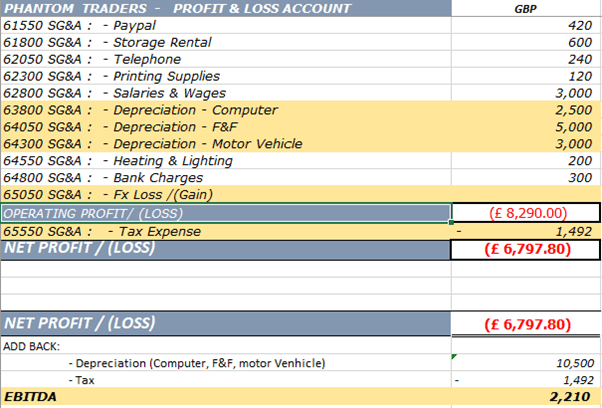

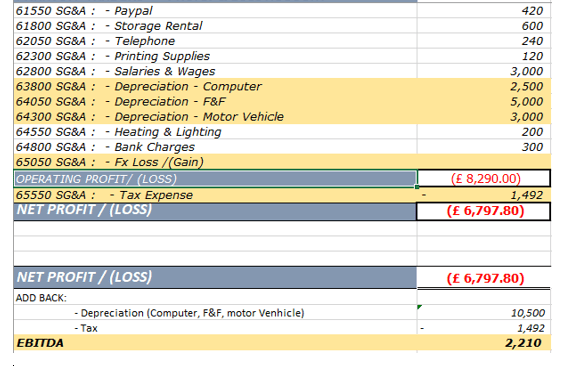

EBITDA – Earnings before income tax, depreciation & amortisation:

Earnings before income tax, depreciation & amortisation is a performance appraisal method used by many Companies to assess their operating performance.

EBITDA is calculated by excluding income tax, depreciation, & amortisation.

Why EBITDA

- EBITDA – Earnings before income tax & depreciation is a key mechanism used by many Corporations to appraise the operating-performance of their divisions & segments.

- Invariably, Cost centre managers complain that their department is subjected to arbitrary allocations. They argue that they do not directly control these costs e.g. depreciation, amortisation, taxes, & foreign exchange losses.

- They argue that these calculations are prepared by the Accountants using arbitrary basis.

- Hence the need to use an alternative method like EBITDA is irreplaceable.

- EBIDTA helps to align all parties on one page as far as performance appraisal system of an Organisation is concerned. This leads to ‘goal congruence’ & avoids tunnel-vision decision-making.

Pros & Cons:

EBITDA is considered to be fairer as far as performance appraisal of Cost Centre/ Sales Managers is concerned, as these individuals are not directly involved in the decision making for working capital management (raising of debt finance) & capital expenditures (buying of assets).

However as far as Lenders & investors are concerned, they may not get full visibility of the business & its operating performance e.g. a business may have a high cost of capital & by deploying EBITDA it may be hiding this.

Similarly, a manufacturing business is likely to have a large asset-base & by deploying EBITDA it will be hiding its true operating position by excluding the depreciation expense.

EBITDA is considered to be closer to Cashflows as it excludes the accounting adjustments (depreciation/amortisation). On the contrary there is an argument that EBIDTA may be inflated by excluding these items depending on the particular industry that Company operates in (manufacturing).

In conclusion, EBIDTA is subject to manipulation on the part of the Company using it. Lenders & Investors may not be able to get full visibility of the operating performance of a Company & hence the Company may not be able to secure a deal that it anticipated (loan/buyout).