SG&A – Selling, General & Administrative expenses are an integral part of any Income Statement. Depending on a particular industry, the average ratio of SG&A to revenue is approximately 10-25%. The Lower the SG&A to revenue ratio, the higher the NPM – Net Profit Margins.

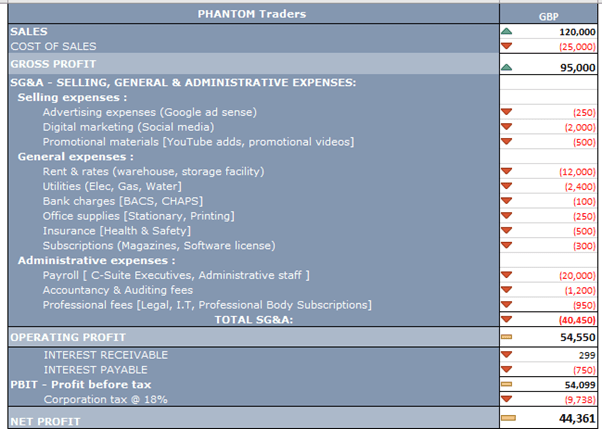

Below is an exhibit showing SG&A expenses of an Online E-store Company.

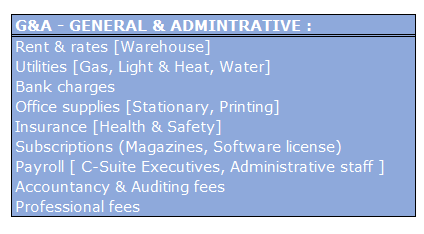

General & Administrative Expenses:

In certain industries, G&A – General & admin expenses are categorised separately within the Income-statement. Internally, the underlying G&A line items are communicated with the relevant Cost Centre Managers & Controllers. These discussions tend to take place between the likes of Finance Managers & Cost Controllers, in order to manage & control costs. As budgets may overrun & costs may be substantially higher than what was agreed & anticipated. Hence the importance of regular communication with finance department cannot be neglected.

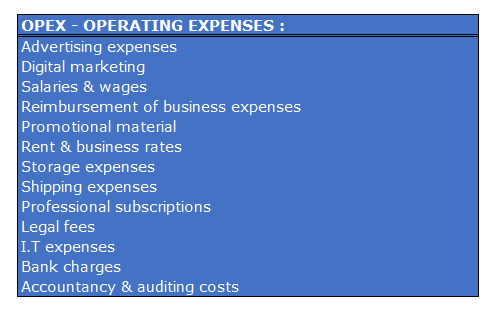

OPEX – Operating Expenses:

OPEX – Operating expenses are incurred to run the daily operations of a Business. Whereas CAPEX – Capital expenditures are incurred to buy the necessary machinery & equipment to be able to produce the goods & services for the Customers & Consumers respectively.

- Companies using ERP systems tend to have more streamlined reports in place to prepare SG&A reports & analyses. Companies using small scale accounting software’s will have to input more time to prepare SG&A reports as the data may not be available in a format required by the Finance department. It may require use of more advance excel functions e.g. macros, array formulas, & scenarios.

- At times the ERP reports may not be 100% streamlined for reporting purposes & finance teams will have to spend lot of time on mining these reports. Especially when these SG&A reports are used to make critical operational business decisions (procurement of goods & services).

- Start-up Companies who raise Capital via Venture-capitalist or PE – Private Equity firms have to ensure that they keep a tight-grip on their SG&A line items. This requires a robust end-to-end control environment.

- As an Accountant your role is to understand the concept of ‘controllability’. When preparing & representing SG&A reports you need to bear in mind that some of the SG&A line items are not directly-controlled by the cost Controllers: –

- e.g. depreciation of fixed assets would depend on the particular depreciation policy & how capex is recognised.

- Foreign exchange losses & gains.

- Prepayments & Utility costs are allocated to various cost centres using arbitrary allocation basis by the finance dept.

- This may lead to a disagreement between the finance department & Cost Controllers. They may argue that the costs allocated to their department are calculated on arbitrary basis.

- When Finance Managers appraise the performance of a particular Cost Centre Controller, they should factor the above discussed points in their appraisal to ensure that a fair performance appraisal system is in place based on controllability & ownership.